NH Employment Security does not have Calendar Year Rates.

Tax Rates for Merit Rated employers are reviewed and determined once a year.

Annual Tax Rate Determination Letters mailed August 29, 2023 for the period 7/1/2023 (Q3/2023) through 6/30/2024 (Q2/2024). Unless there is a major change to the business (such as sale, merger, acquisitions, transfer of workforce) the rate will not change.

However, the Trust Fund Reduction and Trust Fund Inverse Minimum Rate are subject to change each quarter and is listed on the NHES website

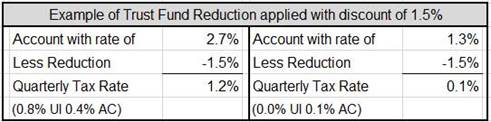

Employers that are in good standing and eligible to take advantage of the Trust Fund Reduction would apply the reduction to the Merit Rate, reducing the rate to as low as .1% (the minimum tax rate for NH Employment Security)

See law change below to UI/AC Rates RSA282-A:87

Newly established Employer accounts that do not qualify for Merit Rating will have a rate of 2.7% less the current quarter Trust Fund Reduction. View list of Trust Fund Reductions: Tax Rate Chart

Quarterly Tax & Wage reports mailed by this agency will indicate the account’s current Tax Rate including any applicable Trust Fund Reduction or Surcharge. View list of Trust Fund Reductions: Tax Rate Chart

Additional information on Trust Fund Reduction and Trust Fund Surcharges: Schedules I-III ![]()

RSA282-A:82

- The fund balance reduction for positive rated employers will be determined based on the balance of the trust fund from the preceding calendar quarter as follows: (effective 1/1/2010)

Trust Fund equals or exceeds $250,000,000 – 0.5% will be subtracted from the contribution rate

Trust Fund equals or exceeds $350,000,000 – 1.0% will be subtracted from the contribution rate

Trust Fund equals or exceeds $400,000,000 – 1.5% will be subtracted from the contribution rate

- Inverse minimum rate –schedule II and schedule III – negative rated employer (employers who’s benefit charges exceeded tax paid) will have additional percentage added to rates depending on Trust Fund balance from the preceding quarter as follows: (effective 1/1/2010)

Trust Fund fails to equal or exceed $250,000,000 – 1.5% will be added to the contribution rate

Trust Fund fails to equal or exceed $350,000,000 – 1.0% will be added to the contribution rate

Trust Fund fails to equal or exceed $400,000,000 – 0.5% will be added to the contribution rate

RSA282-A:87

- Addition of Schedule III for negative rated employers. Will move into schedule III after have been negative rated in Schedule II for 4 or more consecutive years (effective 7/1/2010)

- Effective October 1, 2019 pursuant to RSA 282-A:87 the distribution of quarterly tax paid has been redefined. As a result the maximum AC rate has changed from 0.2% to 0.4%, the minimum AC rate remains at 0.1%. The remainder is allocated to the UI (Unemployment Trust Fund). The net rate has not changed.

For Example: a net rate of 1.2% is now allocated as 0.4% AC and 0.8% UI

Translation Resources and Disclaimer

New Hampshire Employment Security (NHES)

45 South Fruit Street | Concord NH 03301 | 603-224-3311 | 1-800-852-3400

TDD Access: Relay NH 1-800-735-2964